{kind=link}

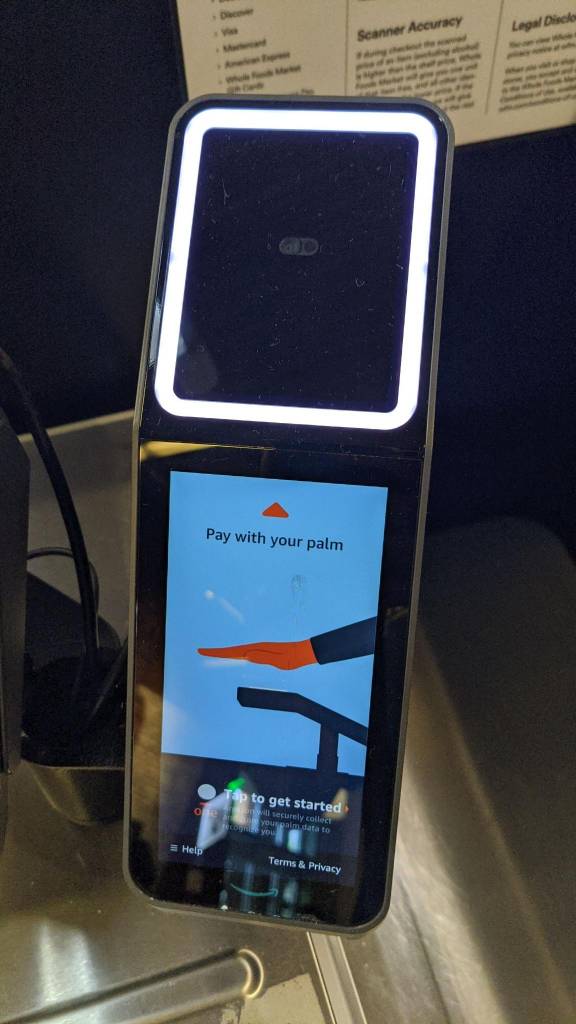

I can only see this going into a very dystopian path. Based on their actions, I don’t trust these companies, their security practices, nor their privacy policies. Why would I give them my biometrics? And my full palm, at that!? Hell no!

I can only see this going into a very dystopian path. Based on their actions, I don’t trust these companies, their security practices, nor their privacy policies. Why would I give them my biometrics? And my full palm, at that!? Hell no!

One scar away from losing access to your ability to pay …

Biometrics can not really be changed. Except maybe through time or trauma (i.e. age or injury). They can be used to uniquely(?) identify a person - except maybe twins - at the expense of anonymity, which has it’s own set of problems.

But because they can not easily be changed they’re a terrible security feature. Once they leak, they’re unusable and you’re hosed. You can’t issue a new palm print for your bank account like you could a new chip card and password.

Also, just because you waved your hand over a scanner does not mean that you approve and consent of the transaction. With tap to pay there were ideas of mobile point of sales devices just tapping on peoples backpacks in a crowded area. You don’t even keep your biometrics markers in your pocket, they’re just out in the open for anyone with a camera. This may be bordering on paranoia, but a few years back (2014) German hackers from Chaos Computer Club took iris scans from Angela Merkel (then Chancellor of Germany) and finger prints of Ursula von der Leyen (then Minister of defense) using nothing but press fotos. Cameras have only gotten better.

TL;DR: Biometrics can be used for identification but should never be used for authorisation.

Biometrics also aren’t great and uniqueness. At least where computers are concerned.

Recently we had one of our customers install fingerprint readers on their points of sale, the idea being any staff member can log in just by touching the pad. Even with only a few hundred staff registered, you get people logging in as each other.

I worked with Kronos, had their top tier biometrics in a 1,000+ employee company.

The data is only as good as the person loading the data.

Some people don’t have good fingerprints.

It was bad enough that of you had a person with a bad fingerprint, Kronos would just take ANY input. It would even tell you if a persons fingerprint wasn’t good enough. It happened fucking constantly.

So either it’s so good you can’t escape it, it is so bad you can’t use it to identify anyone uniquely. It’s literally either a threat or an inconvenience.

Paying with your phone works on the presumption that your phone is locked and you accept responsibility for ensuring your phone wasn’t breached. It uses contactless technology, but it’s still effectively chip and pin as far as your bank is concerned.

Meanwhile, paying with a contactless card is processed as “cardholder not present” where the seller assumes de facto liability and must prove otherwise. Contactless payments were never a new type of card processing, it was a new method but is categorised the same as when mail/phone ordering from a catalogue. The same with online purchases. They were always a step below card & signature or chip & pin. Paying with your phone is the same as chip & pin though, where the onus is on you to ensure the transaction is secure.

Paying with your hand has all sorts of issues making it impractical. You would definitely need an additional confirmation eg PIN, but claiming that your hand is as secure as a traditional card doesn’t lend well to pinning the liability on you. So banks are unlikely to use it.