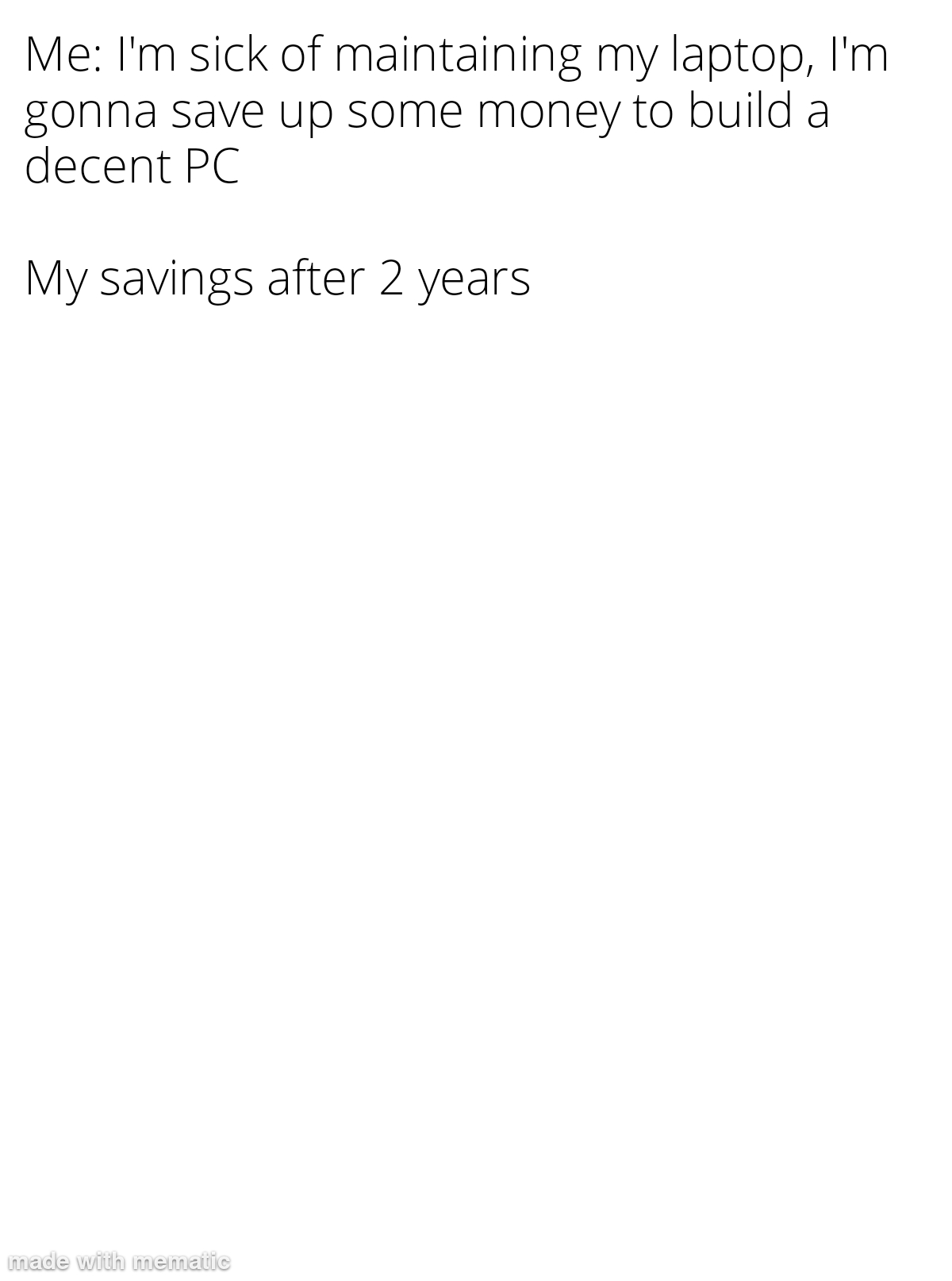

My tablet screen is filthy

Two years later everything is so much cheaper too (except that moment when GPUs went crazy expensive).

I have the impression that soon “any” pc will be totally okay for almost any workload, if it isn’t already.

16GB of RAM, 512GB/1TB of SSD and a hexacore is like cheap nowadays…

‘any pc’ is definitely not good enough. Minimum required specs will just keep rising and rising.I think even stuff like Fifa 23 requires at least an 1060 to run at the bare minimum. In 5-10 years you need a 30 or 40 series card to run games at minimum specs

Only for gaming. Everything else needs basically nothing.

Even gaming is fine if you’re not feeling broken hearted about leaving behind half-assed, broken on release, $70 AAA, Microtransaction riddled masterpieces.

That’s been the case since the second PC though. It’s a lot better now than it was in the mid to late 90’s.

Yeah true gaming seems to be a never ending requirement for more power.

Moore Power’s law

It’s like the interaction between college tuition and the amount lenders will distribute in student loans.

Lenders: “Oh, college is more expensive now…I guess we should increase our borrowing limits for students…”

Colleges: “Oh look, lenders are increasing borrowing limits! I guess that means we can increase tuition!”

Fucking John Cena. Everytime, he takes it all

I’ve found that if I’m “saving” for a purchase, I need something like the adult equivalent of a piggy bank.

Mentally setting aside funds doesn’t work.

Creating a “soft partition” doesn’t work.

The best thing I can do to save (for a small to medium luxury purchase just for myself) is to literally take that money out of my account in cash and put it somewhere safe in my apartment.

If it’s not showing up on my banking app and it’s not in my wallet, it’s like it doesn’t exist. That’s the best way for me to save it.

I do the same. It just work!

The heck? Really? Can’t you just send it to your savings account?

I mean I could, but it’s not as effective. Or rather, it just trades one issue for another.

Basically leaving it in my main spending account means there’s no dividing line between what I’m saving for that purchase and the rest of my spending money. Moving it into my savings, with the rest of my savings, means there’s no dividing line between what I’m saving for this luxury purchase and what I’m saving to, you know, actually save.

In my lizard brain, if I did it that way, from the first $50 I set aside, there would already be enough for the whole purchase in my savings, so there would immediately be the temptation to just dip into my savings and get the item now.

I don’t want to start into the practice of dipping into my savings for luxury purchases anyway, so while yes I could do that, it would simultaneously not solve the issue with just leaving it in my main spending account while also opening up the new can of worms of setting me up for buying luxuries with my savings.

Missing the dollar that fell into the couch. It may be hard to find but it is saved!

It’s not only saved, it’s invested. “I put it into the couch” sounds like an investment hehe

I will assume the savings have gone by being used to buy that PC

You’re optimistic, I respect that.

image isnt loading D:

just gotta wait for 2 years!

F:

What’s on the F drive?

respects.exe

{kind=link}