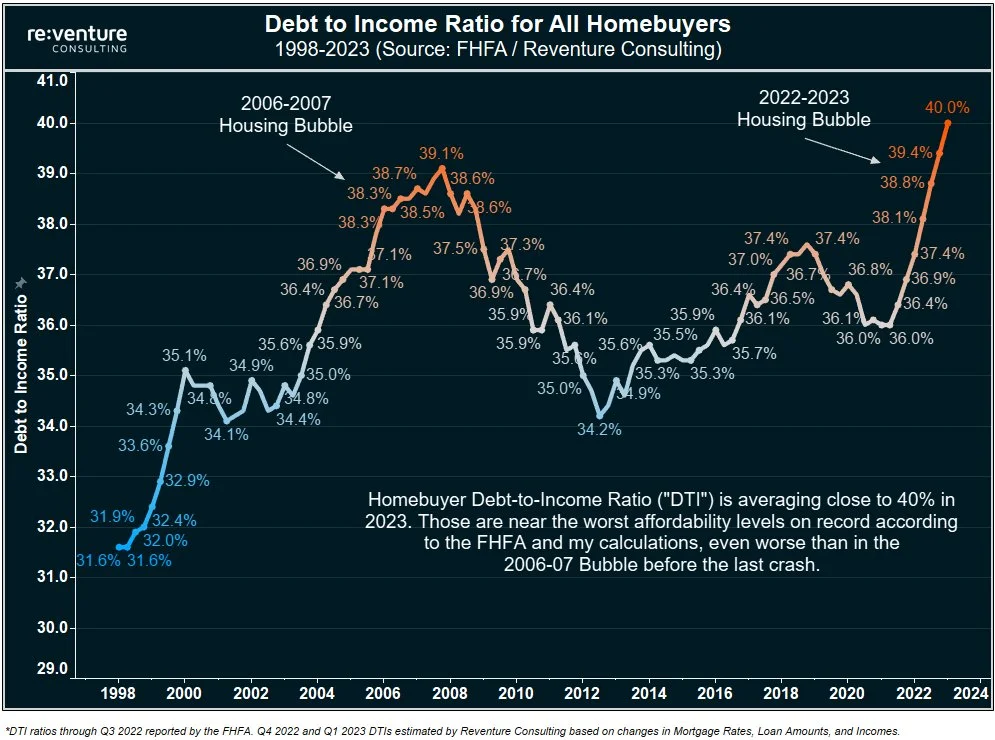

DTI also includes credit card debt and any other outstanding loans, not just the mortgage PITI. It’s still bad, because that means more people are spending almost half their gross paycheck on debt, which leaves very little for food or discretional spending.

The bubble will pop and government will bail out the banks and again fuck the people.

Well yeah, this tracks. House prices have stayed largely the same but interest rates have increased drastically. So you’re getting the same amount of house for huge increase in cost. When you add in wages not keeping pace with inflation and the idea that housing demand is relatively inelastic it absolutely makes sense that people are spending a bigger chunk of less valuable money on housing.

When I bought my house in 2016, the total mortgage (principle, interest, taxes, insurance) was about 18% of my gross. Two jobs later, same house, it’s now 8% of my gross.

House value according to Zillow has doubled since I bought it. As has the interest rates.

Got to crash sometime.