Dave Ramsey is a horrible person. His office is in the Nashville area… There’s always a story in the news about his office and it’s policies

Have a look.

Sorry for the reddit link… https://old.reddit.com/r/nashville/search?q=Dave+Ramsey+&restrict_sr=on&include_over_18=on

i assume the caller is an american

Like how some banks go “save a coffee now, buy a house in a year”

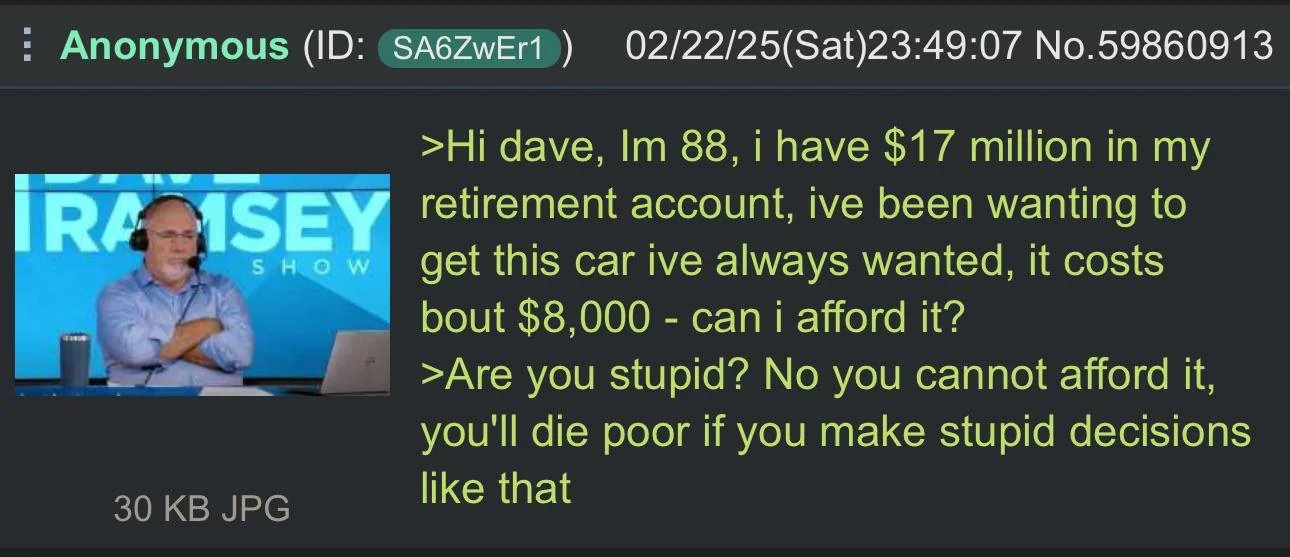

Financial advisor Dave Ramsey Snow

His advice on living within your means usually includes gratuitous torture porn. Yet he always forgets plot armor won’t protect you from financial mistakes.

I haven’t actually directly consumed any of his content but from what I’ve gathered over the years it sort of feels like advice targeting people addicts. The same way it may sound strange to tell someone to never ever ever drink a single drop of alcohol ever but it makes sense if you know they’re a recovering addict.

But at the same time, there’s just some pretty bad advice too. Along with some common sense good advice.

Isn’t dying poor a good thing? I don’t want to live poor, but you can’t take it with you. I’d ideally spend my last dollar right before taking my last breath.

The problem is when you spend your last dollar but still are breathing.

The goal would be to spend my last dollar prior to ending up in a hospital where I die and the medical bills go poof.

Problem is, that you normally don’t know how long you’ll live and cannot plan accordingly.

I know when I’m going to die, because I’m an independent free thinker. I refuse to face my death on anyone’s terms but my own. I intend to live a rich and fulfilling life, watch my family grow, and then end it at a time of my own choosing, after giving all of my grandkids the tools they need to go on without me.

If I died to any means but suicide, I wouldn’t think it fair. You can’t fire me, I quit. It’s my life and I’m going to be in control until the last second.

You goober, even if you’re planning on offing yourself you can still die randomly before that.

The audacity to use the word goober as an insult in a comment this stupid is baffling.

Of course you’re right. Obviously.

Did you not get the point?

That’s true, but irrelevant. We’re talking about managing retirement funds. I’m not going to live longer than my retirement funds last. Dying earlier doesn’t change that.

And if I did die of natural causes, it would be a tragedy. I only want to die by my own hand, I don’t want chance to take my death from me.

If you’re unmarried and have no descendants sure. Although you’re kind of screwing them over, these days, you dying is the only way your kids are ever going to be able to buy a house.

With inheritance taxes in the west not even then.

You can inherit a fair amount without paying inheritance tax.

I would love to have inheritance tax as something to worry about.

It would mean I have millions to leave my family.

Unless you are dying with millions, inheritance tax is nothing.

Exactly. I forget the limit, but it’s something north of $10M before it gets taxed in the US. Not sure about other western countries.

At least in the US inheritance tax really isn’t a thing. It’s only a couple of states that do it, and for federal taxes the estate has to be very large. In 2025 the exemption is 13.99 million per individual from any estate taxes. I certainly have never had a family member with an estate anywhere near that size

at least not without preparation, it’s insane that you have to figure out inheritance in advance or your descendants get screwed. If you set things up properly then here you can inherit a primary residence tax free, but if you don’t set things up then you’re just shafted.

You’re really not. You can do zero planning and as long as the total amount is <$14M, there are no taxes due.

One big difference, however, is pretax investments (IRA and 401K in the US). Sell or convert to Roth before you die and it won’t be an issue at all. If everything is in regular taxable accounts, the beneficiaries even get a step up in basis, so they will only owe cap gains on growth after your death.

Any third rate tax person could figure that out.

Inheritence and/or charity

Dave Ramsey’s advice is only ever applicable to those who are terrible with self-control. If you have at least mediocre self-control, carefully managed debt can be a boon

Dave Ramsey is a bigotted, sexist, racist piece of shit who got rich running mega churches. Ie: scamming people and the government.

He’s fired people because they’ve have children out of wedlock. The whole company is a cult.

Doesn’t that describe pretty much everyone in finance

The average person in finance has different flaws than this particular douchebag.

Hi. I’m an person in finance. Fuck Dave Ramsey. He gives decent financial advice, but the way he shoehorns God into financial matters so frequently was off-putting to me, even when I was a Christian. That, and he’s a racist, bigoted POS.

If you’re in the middle class, his baby steps are somewhat solid stuff, though.

- Learn how to write a budget. There are sites out there to help you with that. Personally, I’ve found I like a spreadsheet best.

- Reconcile your accounts daily. Know where your money has been and where it’s going.

- Squirrel away some cash. A grand ain’t much to have, but it’s a fuckton to owe.

- Don’t drive glitzy cars. A '99 Corolla gets you there just as effectively as a new Tahoe.

- Get out of credit card debt ASAP. If you can’t pay cash for it and you don’t need it, you can’t buy it.

- If debt is crushing you, use what windfalls you can get to pay them down.

- Eat out less. Cook at home more. Not only is it less expensive, it’s generally healthier.

But saving six months’ expenses and paying off your house early…yeah, that’s not feasible for at least 70% people. Especially renters.

The truth is Dave’s screeners do not let anyone through if his program can’t help them. I mean, a single parent in a rural town whose boss won’t pay them enough to survive and whose economic prospects are so limited that “just get a better job” will never work because there aren’t any. People who must rely on the generosity of others to get by and will be completely fucked if they lose their government assistance. Or worse - their job. There’s no financial advice that can help them. Because we live under an economic system that can’t operate if those at the bottom aren’t going through untold suffering and can be helped by “drive an old car, eat beans and rice, and just get a better job.”

At that point, it’s not the fault of the person. It’s the fault of the system. Dave isn’t the problem, but he’s certainly a complication.

There is a British financial advisor who basically says the same thing.

If you can actually manage debt make sure to get some. And then pay it off.

One example: If you get to own a house (that’s paid off) not having debt on it is stupid because you get the lowest interest a regular person possibly can get. Even if everyone else has interest rates up to their mouth you’ll get a rate so cushy investing the money in any index fund will outperform your interest payments.

Disagree, sure you can make more in the open market over time by getting another mortgage on a paid off home.

But that invested money means absolutely nothing if the market has a downturn and you lose your job. Now you’re on the hook to a mortgage you can’t pay and risk losing a place to live.

While on paper you can make more money, it’s very dumb to gamble with things you need to survive. And that’s all any loan is, a gamble that you will be in good health and have the means to pay it back.

That really depends on how risk averse you are, what your payment is, and how stable your job is. For example, my payment is tiny because I got a great rate, bought below my means, and have owned it for several years (so inflation is doing its thing). At this point, I spend more on food than I do on my house.

To mitigate risk, I keep a sizable emergency fund (sustain lifestyle for 6 months), which is currently invested in very safe bonds and money market funds returning a higher rate than my mortgage rate. Why would I pay down my mortgage when I can get more essentially risk free in bonds?

I really like Dave’s question: if you had a paid off house, would you get a mortgage on it? My answer is, hell yeah if I could get the same rate I have now! It’s free money!

If my rate was >5%, I’d pay it down aggressively. But it’s way below that, so I’m holding it until I have enough to retire.

Yeah when he’s talking about debt he means small scale stuff like credit card debt. Basically you buy your groceries on your credit card rather than your debit card even though you could buy them on your debit card.

The reasoning being is that that way you get an extra month of interest before you have to pay out, and you get a good credit score since you always pay off your loans. Which weirdly is actually better than having no credit score at all because you’ve never had any debt.

There is a distinct difference between taking out a loan on your house and saddling it 100% with debt again. Obviously any loan taken out should under all circumstances be one you can comfortably pay back.

Taking out 20k on a 1m home is way different than taking out 20k on a 100k home.

Plus, at least here, if you lose your job the following happens:

- for 2 years you’ll get 80% of your previous paycheck (assuming you worked long enough to qualify, iirc 5 years. if not you get time deducted)

- at the same time as the end of your current employment you have the option to stop/reduce payments on the loan for a time due to special circumstances (technically not mandatory but not bank will give you a large loan without this added insurance, iirc interest will still accrue in this time essentially extending the length of the loan)

Couple that with not being stupid and getting a loan that eats your entire home as backing and you are pretty much safe from any short term disruption in your finances.

To touch on a few other points:

- yes blindly investing is dumb, if the market gives you an uneasy gut don’t invest. That thing has a habit of being wildly irrational until it suddenly and very quickly is forced to realign with reality

- if you have the luck and are in a union that negotiates your wages you will likely receive a “pay rise” aka inflation compensation every couple of years, in such a case a loan as I describe it also makes sense for personal use (in small sums) because inflation will further reduce the interest. Think taking out a loan to renovate a room instead of saving up for it, after everything is properly accounted for the loan backed by property variant will leave you with slightly more money (depending on general interest situation, if interest rates are high but inflation low things might differ)

And worst comes to worst, rent out a room in your house as a sublet and use that to pay exclusively for the mortgage. Any loan you ever take out against an owned home shouldn’t have higher monthly payments than that anyway or it, as you say, turns into an insane gamble no one in their right mind should take.

Plus, at least here, if you lose your job the following happens:

- for 2 years you’ll get 80% of your previous paycheck (assuming you worked long enough to qualify, iirc 5 years. if not you get time deducted)

- at the same time as the end of your current employment you have the option to stop/reduce payments on the loan for a time due to special circumstances (technically not mandatory but not bank will give you a large loan without this added insurance, iirc interest will still accrue in this time essentially extending the length of the loan)

And that’s the difference. Here you just get to be foreclosed on.

So yeah with having reasonable social safety nets in place the idea is a lot more reasonable

The only Ramsay I listen to is Gordon.

The only Gordon I listen to is Freeman

[insert curse words here]

{kind=link}